There are plenty of acronyms when it comes to your personal finances. You likely have come across HSA, COBRA, COLA, ETF, APR, to name a few. But when thinking about your tax situation for the year, there’s one acronym you need to understand: AGI, or Adjusted Gross Income.

Gaining insight into your Adjusted Gross Income, its significance, and the method of calculation can pave the way for a prosperous and tax-smart financial future.

Defining AGI and How It Impacts Your Taxes

Your Adjusted Gross Income is calculated by taking your total gross income for the year and subtracting certain adjustments.

Before delving deeper into the calculation, it’s helpful to understand how your AGI plays a pivotal role in various aspects of your taxes.

A Starting Point for Calculating Your Taxable Income

Your AGI is the starting point to arrive at your taxable income, which is the number the IRS uses to calculate your taxes. Reducing your AGI results in a decreased taxable income, leading to a more favorable tax bill – and who wouldn’t appreciate that?

NOTE: There are several tax charts within The NewRetirement Planner where you can gain further insight into your gross taxable income by source (work income, pensions, social security) as well as your net taxable income by federal tax bracket.

Qualifying for Tax Credits

AGI determines your eligibility for various tax credits. A tax credit directly reduces the amount of tax you owe. It’s a dollar-for-dollar reduction of your actual tax bill.

To qualify for certain tax credits, your Adjusted Gross Income must not exceed specific limits, which vary based on your filing status (e.g., single, married filing jointly, head of household, or married filing separately).

Some credits where this applies include:

- The Earned Income Tax Credit (EITC): for low to moderate income individuals and families

- The Credit for the Elderly or Disabled (The “Senior Tax Credit”): for those 65 and older or for taxpayers under age 65, retired on permanent and total disability, and received taxable disability income

Limitations on Tax Deductions

Tax deductions lower your taxable income for the year. A number of tax deductions you may be able to take advantage of are subject to different AGI limitations:

- Medical and Dental Expenses: If you itemize deductions on your tax return, medical and dental expenses above 7.5% of your AGI are deductible. Therefore, the lower your AGI, the easier it is for more of your medical and dental expenses to clear that 7.5% hurdle to be deductible.

- Donations to Public Charities: Itemized charitable donations to public charities you can deduct in a tax year are capped at a percentage of AGI. For contributions of non-cash assets held more than one year, the limit is 30% of your Adjusted Gross Income. Your deduction limit will be 60% of your AGI for cash gifts.

Impact on Social Security Taxation

The IRS uses a formula to determine if a portion of your Social Security benefits is subject to federal income tax. This formula is often referred to as the “provisional income” formula.

Provisional income is calculated by adding your AGI, tax-exempt interest (such as interest from municipal bonds), and 50% of your Social Security benefits.

Therefore, an increase in your AGI can subject more of your Social Security income to taxation.

Understanding the Parts of Your AGI: Gross Income and Above-the-Line Deductions

Now that you have an understanding of how AGI impacts certain tax opportunities, you may be curious on what exactly makes up your Adjusted Gross Income.

An Explanation of Gross Income

Before we can arrive at your Adjusted Gross Income, it’s important to understand your gross income. Gross income is generally the starting point for the federal individual income tax return (Form 1040). The IRS defines gross income broadly as all income from any source unless specifically excluded by the tax code.

Common exclusions from gross income

The general rule is all income is taxable, unless specifically excluded by tax law. These non-taxable income sources are called exclusions – they are exempt from tax and not included in gross income.

Some of the more common types of income that may be excluded from gross income include:

- Most retirement plan salary deferrals, like pre-tax 401(k) contributions

- Child support payments received

- Gifts received

- Life insurance death proceeds

- Interest received from municipal bonds

Common sources of gross income

The amount of income remaining after removing any exclusions is your gross income. Some common sources of gross income include:

- W2 wage income (earnings you receive from an employer) and other earned income, like bonuses and commissions

- Self-employment (“Schedule C”) income

- Social Security benefits (up to 85%)

- Pensions

- Retirement account withdrawals

- Rental income and royalties

- Capital gains, dividends and interest income received

NOTE: The NewRetirement Planner empowers you to track numerous sources of gross income, ensuring an accurate representation of your taxable income for the year.

Calculating your gross income: an example

It may be helpful to look at an example to better understand your gross income calculation.

In 2023, Jane received the following:

- A salary of $150,000

- Dividends of $5,000

- Tax-exempt interest of $1,000

- A gift of $15,000 from her mother

Her total income for 2023 is $171,000, because total income is based on income from all sources. However, her gross income reported on her tax return would be $155,000, the sum of the $150,000 salary and the taxable dividend income of $5,000.

The remaining $1,000 of tax-exempt interest income and $15,000 gift from her mother is excluded from gross income.

Deductions and Their Impact on AGI

After adding up your gross income, it’s time to review your tax deductions for the year.

Two primary categories of deductions with respect to AGI include:

- Above-the-Line Deductions: Come off your gross income first, before reaching your AGI. These can often be referred to as deductions for AGI.

- Below-the-Line Deductions: Come after your AGI has already been calculated. These are referred to as deductions from AGI and can be either your standard deduction or the total amount of your itemized deductions, whichever you choose.

- The standard deduction is a fixed dollar amount that taxpayers can subtract from their AGI.

- Itemizing deductions involves listing out individual expenses that you want to write off on your return, like medical and dental expenses and mortgage loan interest.

In calculating AGI, you may reduce gross income by above-the-line deductions. Some of the more common deductions include:

- Unreimbursed expenses for educators who work in schools

- Contributions to a health savings account (HSA) (outside of payroll)

- Moving expenses for members of the Armed Forces

- The deductible part of self-employment tax

- Contributions to self-employed retirement plans, like SEP and SIMPLE IRAs

- Health insurance premiums for self-employed people

- Eligible contributions to a traditional IRA

- Student loan interest

Arriving at Your Adjusted Gross Income

With a handle on gross income and above-the line-deductions, it may be helpful to walk through an example of calculating AGI:

Joe and Jane Smith are in their early 60s and file their taxes jointly. They have the following gross income:

- Joe’s taxable wages from Form W-2: $100,000

- Jane’s taxable wages from Form W-2: $175,000

- Interest income: $10,000

- Dividend income: $6,000

Their total gross income is $291,000.

Their above-the-line deductions include:

- Health Savings Account contribution (made outside of payroll): $7,750

- Educator Expenses: $300 (Joe is a teacher)

Their total above-the-line deductions are $8,050.

Their AGI would be calculated as follows:

- Gross income: $291,000

- Less above-the-line deductions: $8,050

- Equals Adjusted Gross Income: $282,950

Locating Your Adjusted Gross Income on Your Tax Return

If you utilize a tax professional or tax software to handle your taxes yourself, you fortunately don’t need to delve too deeply into the details of calculating your Adjusted Gross Income independently.

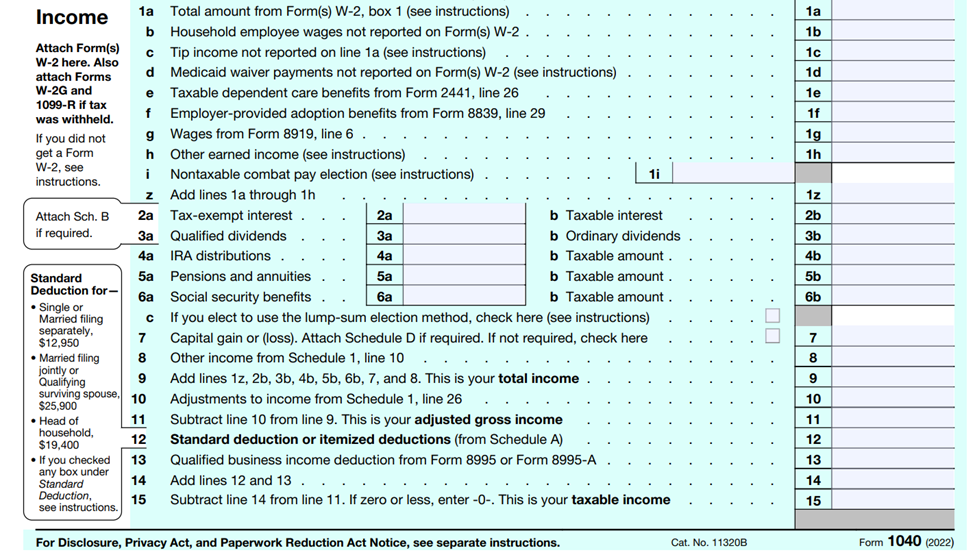

To find your Adjusted Gross Income on your tax return, you can identify it on Line 11 of Form 1040. Here’s the front page of the 2022 Form 1040 where your AGI can be located:

Knowing Your AGI is Helpful, but Having An Overall Financial Plan Is Critical

Calculating your AGI (or being able to locate it on your tax return!) is helpful, but having a well documented overall financial plan is key to your overall financial well-being.

The NewRetirement Planner lets you plan for one of the biggest life transitions you may encounter: your retirement. It offers user-friendly features and empowers you to manipulate numerous variables, allowing you to customize a retirement plan that aligns with your preferred lifestyle and financial capabilities. You can set different levels of income, different levels of expenses, understand potential lifetime taxes and so much more.

With a solid grasp of your AGI and the use of this Planner in your retirement planning, you’re paving the way for a prosperous financial journey ahead!