It’s everyone’s favorite time of the year: tax season! Ok…that may be an exaggeration, but either way, it’s likely that you will come across tax terms that may have you scratching your head.

Taxes are a certainty every year, so having a better understanding of some jargon can make the whole topic a little less daunting.

Navigating the U.S. Federal Income Tax System

You are NOT alone if you don’t know the difference between your marginal and effective tax rate. However, understanding these rates is essential for effective tax planning.

Along with gaining insight into how much of your income is going to taxes, you’ll also be able to make better decisions around tax planning opportunities.

Marginal tax rate

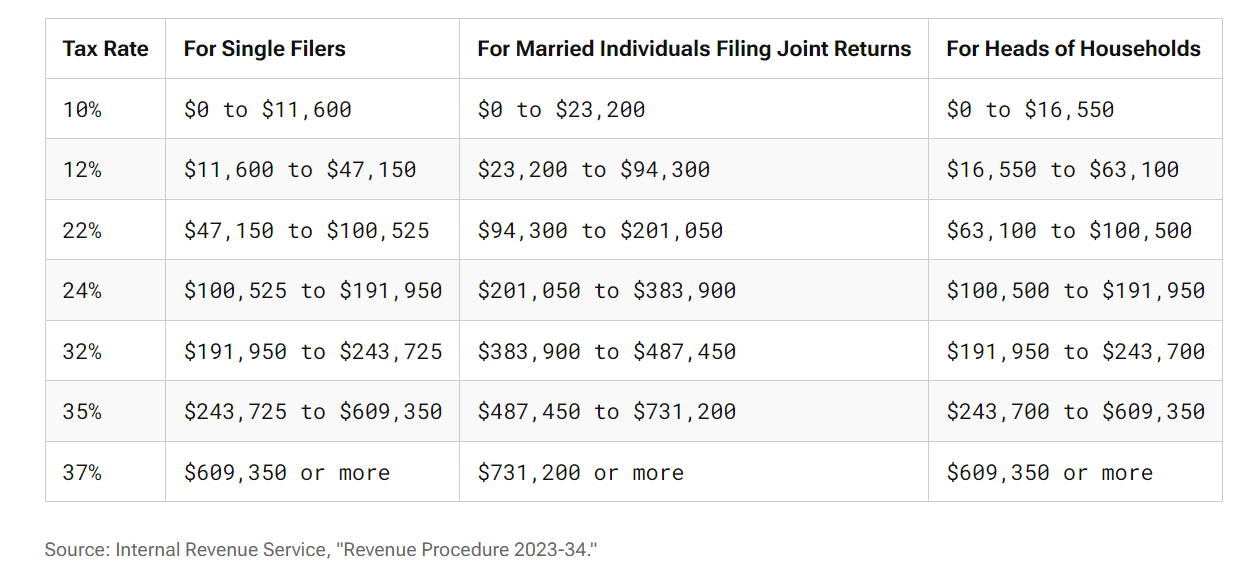

The U.S. federal income tax system is progressive. This means tax rates increase as your taxable income increases.

The tax bracket into which your last dollar of income falls determines your marginal tax rate. However, you don’t pay that higher marginal tax rate on your entire income. You only pay the higher rate on the portion of income that actually falls within that top tax bracket. The income earned in the lower brackets gets taxed at the corresponding lower rates.

The tax brackets for 2024 are as follows:

Examples of marginal tax rates in action

Let’s take a look at a simple example using 2024 figures to help explain this concept further:

- Tax Filing Status: Married Filing Jointly

- Total Gross Income (before applying any deductions): $220,000

- Standard Deduction (itemized deductions were lower so the standard deduction was claimed): $29,200

- Taxable Income: $190,800

Based on the 2024 tax brackets, you would pay:

- 10% on your first $23,200 of income: $2,320

- 12% on your next $71,100 of income ($94,300 – $23,200): $8,532

- 22% on your next $96,500 of income ($190,800 – $94,300): $21,230

- Total tax due: $32,082

Your marginal, or highest, tax rate would be 22% in this example.

Marginal tax rates serve an important role when you are making certain tax-management decisions, like if it makes sense to do a Roth conversion as an example, among other planning opportunities.

If you head over to Insights > Taxes in the NewRetirement Planner, the Net Taxable Income by federal Tax Bracket chart will give you a better idea of the margin tax rate that applies to your specific financial situation.

Effective tax rate

While your marginal tax rate represents the highest tax bracket your taxable income puts you in, the effective tax rate is the total dollar amount of your tax liability as a percentage of your taxable income. In other words, it’s the average tax rate that you pay on all of your taxable income.

Your effective tax rate is the total amount you pay in taxes for the year divided by your taxable income:

Effective tax rate = Total tax ÷ Taxable income

Going back to the example above for calculating your marginal tax rate:

- Taxable Income: $190,800

- Total Tax Due: $32,082

- Effective Tax Rate ($32,082 ÷ $190,800) = 16.8%

In this example, the marginal tax rate was 22%, but the effective tax rate is lower, at 16.8%.

Effective tax rates are helpful in gaining a better understanding of the percentage of your total income that is allocated to taxes.

Making Sense of Tax Documentation

If the idea of preparing your tax return isn’t already anxiety-inducing enough, receiving or coming across mysterious tax document lingo doesn’t mitigate those feelings.

Form W-4

If you’re employed in the United States, you’re likely familiar with the W-2 tax form, which you receive early in the year and summarizes your annual earnings and the taxes deducted by your employer for federal, state and local purposes.

Meanwhile, the Form W-4, an IRS document, is filled out when you are an employee to guide your employer on how much federal tax should be withheld from each paycheck. Completing this form accurately is essential as it prevents both overpayment, increasing your take-home pay, and underpayment, avoiding surprising tax bills or penalties.

It’s not uncommon to fill out a W-4 as a new hire and then never come across it again. However, there are times where it can make sense to revisit the W-4, such as:

- A change in tax filing status (e.g. married filing jointly to single)

- Obtaining a second job

- Going from a dual-income household to single income household

- A new addition to the family (e.g. birth of a child)

- Eligibility for substantial tax credits

- Buying a new home

Revising a W-4 can feel daunting, but there are helpful resources out there to assist with the process. Keeping your Form W-4 updated ensures that your withholding accurately reflects your current tax situation.

1099

Filing your taxes is never an exciting activity to look forward to each year. Whether you work with a tax professional or tackle it on your own, it can be stressful gathering the necessary documents to prepare your taxes accurately, especially when you may not have a full understanding of the documents you are receiving.

A common tax document is a Form 1099. This tax document reports income you receive from sources other than an employer. There are many different types of 1099 forms, each with its own unique reporting requirements.

The most common types of 1099 forms include:

- 1099-DIV: income received through dividends and other stock distributions (generally $10 or more)

- 1099-INT: interest income from a bank or another financial institution (generally $10 or more)

- 1099-B: proceeds from the sale of stocks, mutual funds, ETFs and other types of financial transactions, plus the sale date and other information

- 1099-R: distributions from pensions, annuities, retirement or profit-sharing plans, IRAs, and insurance contracts and will provide information on any taxes withheld from the distribution

- 1099-SA: withdrawals from your HSA (distributions for qualified medical expenses are not taxable)

You should look out for the 1099s that are applicable to your financial situation in January and February of each year as these are essential tax documents in preparing an accurate tax return.

NOTE: Reviewing your 1099 from a taxable investment account can be helpful in applying an appropriate turnover rate for tax purposes to these types of accounts in the NewRetirement Planner.

Reducing Your Tax Bill

A deduction, a credit…it may sound simple but unless you’ve recently attended an accounting class, it’s worth revisiting these common terms you may come across when discussing lowering your taxes.

Tax deductions

Who doesn’t like talking about reducing your tax bill?

One of the ways to do this is through a tax deduction, which is an expense that can reduce your taxable income, therefore reducing your overall tax liability. Tax deductions are subtracted from your income before taxes are calculated, which reduces the amount of income that is subject to taxation.

There are two main types of tax deductions:

- Standard Deduction: A fixed dollar amount set by the IRS that can be claimed when you do not have enough qualified expenses to itemize

- In 2024, the standard deduction varies based on your filing status with Single and Married Filing Separately at $14,600, Married Filing Jointly at $29,200 and Head of Household at $21,900

- Individuals over age 65 may claim an additional standard deduction of $1,950 for single or head of household filers and $1,550 for married filing jointly or separately filers

- Itemized Deductions: Specific expenses that can be claimed on your tax return, like medical and dental expenses and mortgage loan interest, among others

The Planner estimates if you would be better off itemizing deductions or using the standard deduction both at the Federal and State levels in each year of the simulation.

While tax deductions reduce your taxable income, a tax credit can be even more valuable, which we’ll discuss next.

Tax credits

A tax credit is another beneficial tool for reducing your overall tax liability.

A tax credit directly reduces the amount of tax you owe. It’s a dollar-for-dollar reduction of your actual tax bill, making it an even more valuable tool than a deduction for minimizing your tax obligation.

There are two primary types of tax credits:

- Refundable: reduce your tax liability to below zero, which means you may receive a refund

- Non-refundable: reduce your tax liability to zero but cannot result in a refund

Tax credits vary widely, both in terms of their amount and types, and these can change from one tax year to the next. It’s important to thoroughly review any applicable tax credits when you are preparing to file your annual tax return.

Consider Taxes as Part of Your Charitable Giving Strategy

Who wouldn’t want to give to charity and also save on taxes? It’s a win-win situation! But, of course, there’s a lot of different terminology when it comes to saving taxes through charitable giving tools.

Donor Advised Fund (DAF)

If you’re feeling charitably inclined and have explored different avenues for giving, you may have come across information on a Donor Advised Fund, or DAF.

With a Donor Advised Fund, you establish an account, contribute funds, and then decide on the investment strategy while also initiating grants to chosen charities. The grants must be directed to qualified charitable organizations, and you have the flexibility to arrange one-time gifts or recurring gifts. For example, you could deposit $20,000 into the fund and elect that you would like to distribute $5,000 to your chosen charities over a span of 4 years.

When you make a contribution to your DAF, you get an immediate tax deduction. This benefit can be particularly valuable in years when your taxable income is higher. By doing so, you may surpass the standard deduction threshold and itemize your deductions to further minimize your tax bill for the year.

DAFs offer a flexible, easy to set up and cost-effective approach to charitable giving.

Qualified Charitable Distribution (QCD)

Another common strategy for charitable giving is a Qualified Charitable Distribution, or QCD.

With a QCD, you are taking a distribution from your IRA and giving it directly to a qualified charitable organization. The distribution must be made directly by the trustee of the IRA to the charity. An IRA distribution, like an electronic payment made directly to the IRA owner, does not count as a QCD.

In 2024, individuals aged 70.5 and older can contribute up to $105,000 per year to one or more charities. For a married couple, if both spouses are age 70.5 or over when the distributions are made and both have IRAs, each spouse can exclude up to $105,000 for a total of up to $210,000 per year.

A QCD is a valuable strategy from a tax standpoint for the following reasons:

- You don’t report QCDs as taxable income

- You don’t owe any taxes on the QCD, even if you do not itemize deductions

- You can satisfy your annual Required Minimum Distribution (RMD)

- You can reduce RMDs in future years by reducing the balance of the IRA

NOTE: When choosing to make a QCD, confirm the receiving organization is qualified to accept QCDs.

Simplifying Tax Lingo Related to Investments

It’s important to keep investing simple, but it can be difficult when taxes come into play with most investment decisions.

Tax-loss harvesting

Tax-loss harvesting is a potential strategy relating to investments within a taxable brokerage account.

It involves selling investments that have decreased in value or are underperforming, thereby realizing a capital loss, and replacing the investment with a highly correlated alternative. You would then use that loss to offset any realized capital gains from selling other investments, with the goal of reducing your overall tax liability.

If there are no realized capital gains to offset, up to $3,000 per year in investment losses can be used to offset your wages, taxable retirement income and other ordinary income (for married individuals filing separately, the deduction is $1,500). If you realize more than $3,000 in losses in a single year, you can carry over the excess amount to offset capital gains and income in future years.

Wash sale

It wouldn’t be prudent to talk about tax-loss harvesting without being aware of the wash sale rule.

The wash sale rule prohibits the selling of securities, such as stocks or bonds, at a loss, buying back those same or “substantially identical” shares within 30 days before or after the sale, and deducting such loss for income tax purposes. Since it’s 30 days before or after the sale, it is actually a 60-day prohibited period during which the loss may not be deducted.

If you’re thinking about tricking the IRS by including your spouse in the transaction, think again! The wash-sale rule applies to both you and a spouse as if you were a unit. For example, if you’re thinking of selling a security in a taxable brokerage account at a loss and then having your spouse buy it back in their IRA, it would still be considered a wash sale.

The purpose of the wash sale rule is to discourage you from selling securities to take a tax loss and then turning right around and buying them back.

Keep Up-to-Date with Tax Legislation

Along with tax jargon, to make things even more complex, tax laws always seem to be changing from year to year. It’s important to be aware of potential changes to your tax situation on the horizon.

The Tax Cuts and Jobs Act (TCJA)

In 2017, the Trump administration signed into law a significant piece of tax legislation, The Tax Cuts and Jobs Act (TCJA).

TCJA brought about extensive revisions to the U.S. tax code, including temporarily lowering individual income tax rates, an increase in the standard deduction, a reduction in the corporate tax rate, and changes to various deductions and credits.

Unless Congress takes action, several of the temporary changes brought on by TCJA for individual taxpayers are set to expire on December 31, 2025. One of the bigger changes would involve the individual tax rates reverting to their 2017 levels:

- The 12% rate could return to 15%

- The 22% rate could return to 25%

- The 24% rate could return to 28%

- The 32% rate could return to 33%

- The 37% rate could return to 39.6%

Given taxes play such an essential role in your retirement planning, the NewRetirement Planner allows you to switch between and simulate various projections using either the existing lower tax rates or the potential return to the higher rates, starting in 2026.

Learn more about TCJA or try out the tax rate toggle in the NewRetirement Planner in My Plan > Assumptions.

Gain Insights on Your Tax Situation with the NewRetirement Planner

With a better understanding of some tax terms, you may feel more equipped to tackle your taxes this year. However, tax planning isn’t a one and done event; it’s an ongoing process.

The NewRetirement Planner enables you to see your potential tax burden in all future years and get ideas for minimizing this expense. As your understanding of taxes deepens, you’ll feel more empowered and confident about the success of your financial plan.